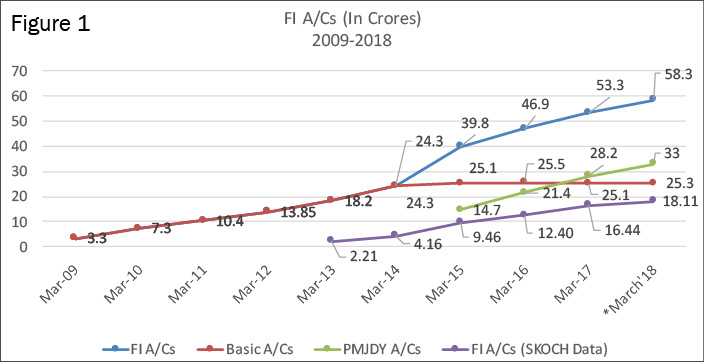

From a poorly banked to an almost universally banked country at the household level is the most laudable achievement of the Financial Inclusion (FI) initiatives of the government since 2014. Financial inclusion gets a big push under Pradhan Mantri Jan Dhan Yojana (PMJDY), wherein 33 crore FI A/Cs have been added in the largest concerted effort ever to push the total number of FI A/Cs to 58.3 crore that serve the purpose of FI, says a report by SKOCH Group entitled, “PMJDY Drives Financial Inclusion Home: A Performance Analysis of PMJDY”.

The report, authored by Sameer Kochhar, Chairman, SKOCH Group and Rohan Kochhar, Director of Public Policy, SKOCH Group says that this is the biggest ever jump – 2.4 times or 140% – in the number of financial inclusion accounts opened. Based on the SKOCH Sample Data, the six sampled banks had a total of 18.11 crore FI A/Cs in December 2017, up from 4.16 crore FI A/Cs in March 2014—an increase of 4.35 times (Figure 1).

Overall there were 24.3 crore FI A/Cs in March 2014, which touched 58.3 crore by end of March 2018. The figure had already touched 56 crore as on December 2017, out of which, 25.3 crore accounts were Basic Accounts. Increase in number of active FI A/Cs shows a strong momentum in usage of banking services.

Rural Financial Inclusion

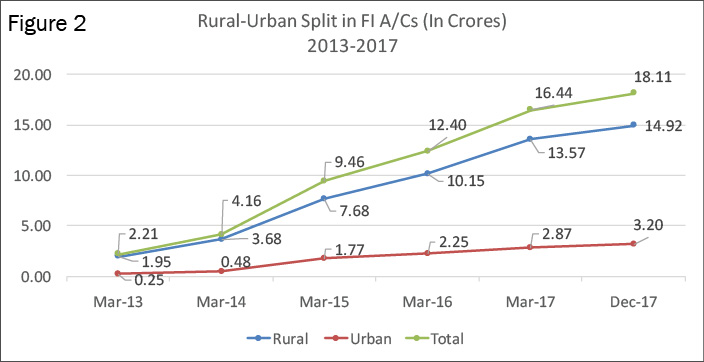

Of the 99.95% coverage of households under PMJDY, Rural FI A/Cs increased to 15 crore in December 2017, up from 3.68 crore in March 2014 – a jump of 4.15 times or whopping 305%. Urban FI accounts during the same period leapt to 3.26 crore from 0.48 crore – an unprecedented jump of 6.6 times or 566%. This makes India an almost universally banked country at the household level (Figure 2).

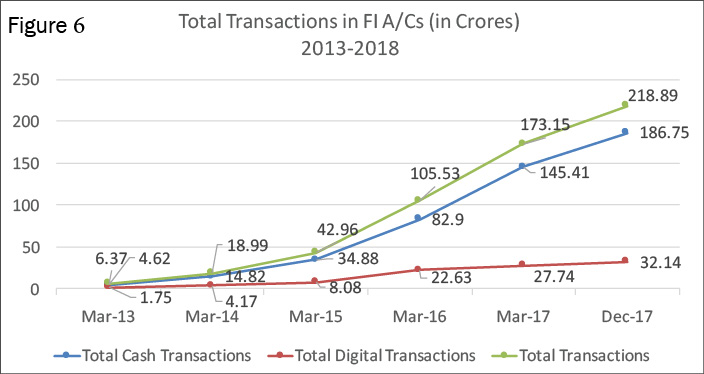

Not only have the number of accounts soared, the number of transactions in FI A/Cs have also exponentially gone up and that these have registered a jump of 11.52 times in the quantum of transactions. It is particularly noteworthy that the Digital Transactions have spiralled 7.7 times – up from 4.17 crore in March 2014 to 32.12 crore in December 2017. The overall transactions have been estimated to go up by six times, indicating heightened activity in FI A/Cs, the report says.

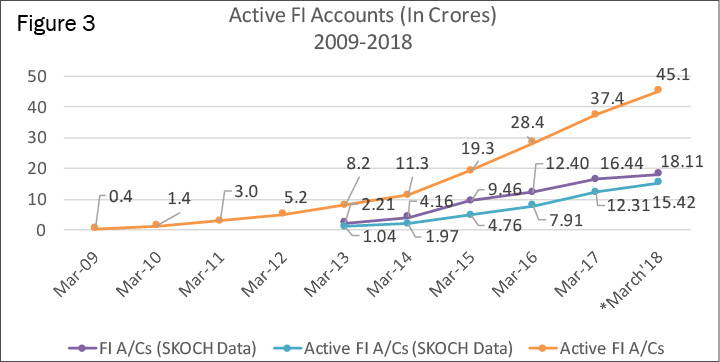

Based on the SKOCH Sample Data, the six banks have a total of 18.11 crore FI A/Cs, 85% of which, i.e., 15.42 crore accounts are active. Overall there were 11.3 crore active FI A/Cs in March 2014, which is expected to touch 45.1 crore by March 2018. This figure touched 39.2 crore as on December 2017—an increase of 4 times (Figure 3).

Rural Financial Inclusion

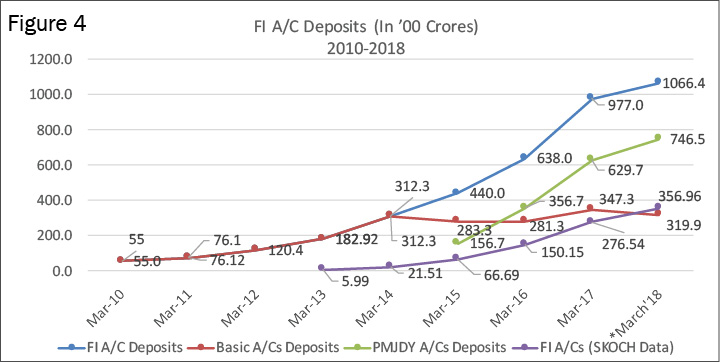

Rural India is saving more, for which, the credit goes to FI initiatives of the Government of India (GoI). Overall there were Rs 31,230 crore in deposits across 24.3 crore FI A/Cs in March 2014. Four years hence, this number has jumped by 3.14 times to Rs 106,640 crore in March 2018. Nearly 70% of this or Rs 74,650 crore are in 33 crore PMJDY accounts (Figure 4).

The shows an exponential improvement in saving habits and capital formation among people who were until recently unbanked and excluded.

As per the SKOCH sample data, the average balance in Rural areas went up from Rs 514.40 in March 2014 to Rs 1695.24 in December 2017. Similarly, for Urban areas it is estimated at Rs 3,251, up from Rs 537.5 during the same period.

The report says there is a similar 3.41 times jump in income of banks on account of PMJDY accounts. At 3% spread, it is expected to be Rs 3,199.3 crore in March 2018, up from Rs 936.9 crore in March 2014. The upward trend is suggestive of the fact that the money deposited in PMJDY accounts is still in the system and that the criticism that PMJDY accounts were misused during demonetisation is unfounded since the money deposited by PMJDY account holders is still in the system. In fact, if the accounts were being misused, the money would have exited such accounts long time ago.

24 crore RuPay Cards

Of 33 crore FI A/Cs added since 2014, 24 crore now have a RuPay Card. Out of these, 13.2 crore or 55% have been used at least once.

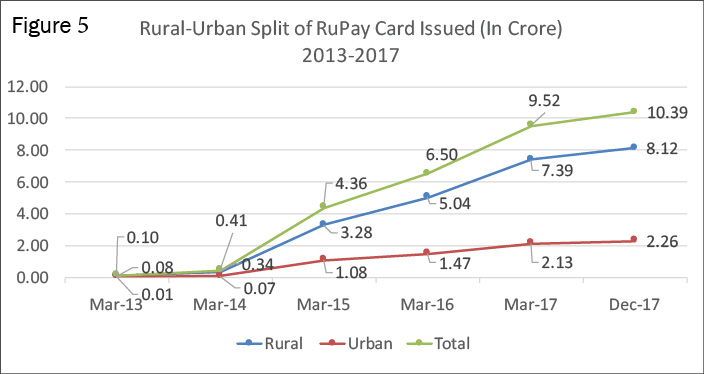

The report says that the necessary infrastructure for a transition to digital payments is in place. It indicates that the Rural FI A/Cs, as per the SKOCH sample data, which stood at 14.92 crore in December 2017, have a far larger share of RuPay Cards than Urban FI A/Cs at 3.20 crore in December 2017. This split stands at 78.22% in Rural areas and 21.78% in Urban as in December 2017 (Figure 5).

Transactions

Overall digital transactions have risen from 4.17 crore in March 2014 to 32.12 crore in December 2017, reflecting a jump of 7.7 times, report highlights. This is also indicative of heightened economic activity in FI A/Cs.

Similarly, cash transactions have also shown an upward trend, up from 14.82 crore in March 2014 to 186.75 crore in December 2017, pointing towards a 12.6 times growth in Cash Transactions (Figure 6).

Micro Insurance Success

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) and Pradhan Mantri Suraksha Bima Yojana (PMSBY) have been successful in providing a social security safety net to those who were not only ‘unbanked’ but also ‘insurance excluded’ prior to 2014. According to the Report, FI A/Cs are clearly out-performers in insurance. While LIC is leading in PMJJBY, New India Assurance leads in PMSBY.

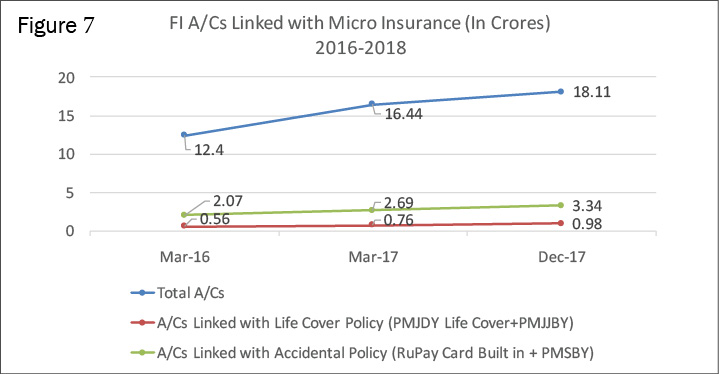

The report says, out of 33 crore FI A/Cs, 18.4% of FI A/Cs had linkage with accident insurance and 5.4% of these accounts had life insurance linkage. This, when the overall insurance penetration in India is merely 3.7% (Figure 7).

Out of the SKOCH sample study data, 18.11 crore FI A/Cs, 3.34 crore had accident insurance and 0.98 crore had life insurance cover. The insurance includes cover bundled with RuPay Card as well as accounts opting for PMSBY and PMJJBY. Out of these accounts only about 0.1 crore were found to be linked with Pension schemes – Atal Pension Yojana (APY) and Swavlamban Yojana, report said.

Channel Expansion

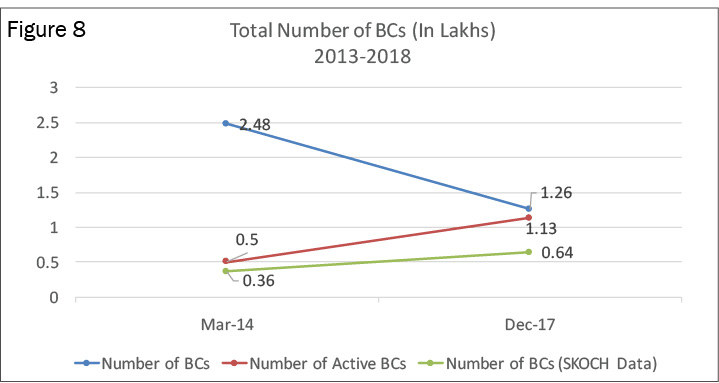

The number of rural bank branches has seen a steady increase from 33,370 in March 2010 to 50,880 in March 2017. This is indicative of greater rural penetration by banks. The number of Banking Correspondents (BCs) has dwindled from 2.48 lakh in March 2014 to 1.26 lakh in December 2017. However, the number of active BCs has increased significantly since March 2014 when almost 80% BCs were inactive to December 2017 where more than 90% of the 1.26 lakh BCs are active (Figure 8).

Based on the SKOCH Sample Data of six banks, of the 64,000 BCs studied, it came to light that a total of Rs 429.99 crore credit and Rs 23.29 crore recovery business was done through them from March 2013 till December 2017. This is a significant increase from only Rs 1.64 crore credit and Rs 2.25 crore recovery business conducted through BCs as reported for March 2015. On the basis of 64,000 BCs studied, the total credit income comes out to be Rs 8.03 crore, total recovery income Rs 1.32 crore and total income from other sources comes out to be Rs 542.1 crore. Average monthly income (Fixed & Variable) of a BC as estimated by Microsave is Rs 5,775.

Recommendations

- PMJDY accounts should be mandated for Direct Benefit Transfer (DBT).

- Cards issued to PMJDY accounts should have a built in credit limit of Rs 500 adjusted against DBT.

- Credit should be made available @14% or higher.

- The credit limit should go up gradually.

- A small savings product is urgently required.

- Exchange Traded Funds, e.g., Gold and Silver should be offered.

- Having largely met the banking objectives, new focus areas should be as follows:

- Increase transactions, create credit history, improve BC income.

- Financial Literacy needs urgent attention.

- Link to markets and other products that offer long-term financial security including post retirement.

- Pension scheme to be kick started.

- The horizon should be expanded to include all financial services.

Methodology

- SKOCH has been studying Financial Inclusion before the inception of government schemes in this sector in 2004. It has periodically published research on the performance of these schemes and made recommendations for improvements. Several of these recommendations have been implemented. The SKOCH Knowledge Repository has been extensively used for the current analysis.

- For the present study, primary data on FI A/Cs was sought from six public sector banks, namely, SBI, Allahabad Bank, Vijaya Bank, United Bank of India, Punjab & Sind Bank and Bank of India.

- These banks together account for 54% of the PMJDY accounts. Data from these banks has been extrapolated and used to estimate overall scheme numbers wherever relevant. Most data is available up to December 2017 or early-February 2018. At places this has been extrapolated to March 2018. All such primary data is referred to as SKOCH Sample Data in this report.

- Several rounds of interviews and conferences were conducted across stakeholders.

- Extensive interviews were conducted even outside these banks, which provided the data.

- Additionally, data was accessed from RBI website (https://www.rbi.org.in) and PMJDY website (https://pmjdy.gov.in).

Summary

• India now has 58.3 crore Savings & Bank Deposit Accounts

• Active Financial Inclusion Accounts (FI A/Cs) have shot up to 45.1 crore by March 2018 – 4 times jump

• Heightened Economic Activity – 11.52 times jump; Digital Transactions up 7.7 times

• Overall there were Rs 31,230 crore in deposits in FI A/Cs in March 2014; Rs 1,06,640 crore by March 2018 – 3.14 times jump. 70 pr cent of these are in PMJDY A/Cs

• 24 crore FI A/Cs have a RuPay Debit Card – 21 times jump; 55% used at least once

• Based on SKOCH Sample Data of 6 banks, total RuPay cards issued in Rural areas witnessed a massive jump of 23.71 times from 0.34 crore in March 2014 to 8.12 crore in December 2017

• The total RuPay cards issued in Urban areas increased by 32.98 times from 0.07 crore to 2.26 crore within the same period

• 18.4% of FI A/Cs have Accident Insurance; 5.4% have Life

• Growth in Bank Branches in Rural areas – up from 33,370 in March 2010 to 50,880 in March 2017

• 90% of 1.26 lakh Banking Correspondents (BCs) are active